Dollar General closed fiscal year 2024 with total revenue of $40.6 billion, up approximately 5 percent year over year, and same store sales growth of 1.4 percent. The headline numbers reflect a year of strategic reset under returning chief executive Todd Vasos, who came out of retirement to lead the company through what is best understood as a corrective cycle. For consumer brands evaluating the small box value channel, the strategic context shapes what the next twenty four months will look like for vendor relationships.

The strategic reset context. Dollar General entered fiscal 2024 with multiple operational pressures, including elevated inventory shrink, store labor challenges, and supply chain inefficiencies that had accumulated over the prior two years. The leadership reset focused on operational fundamentals, store standards, inventory accuracy, and the foundational systems that support the small box high frequency model. The corrective work produced operating margin pressure during the year but positioned the company for a healthier execution baseline going forward.

The customer base dynamics. The Dollar General customer skews meaningfully toward households earning less than $40,000 annually, which represents one of the most pressured consumer segments in the current economic cycle. The same store sales growth of 1.4 percent was driven by traffic recovery as the year progressed, with the back half of the year delivering meaningfully better comparable performance than the front half. The strategic question for the channel is whether the value oriented customer continues to recover or whether macro pressure extends the soft cycle.

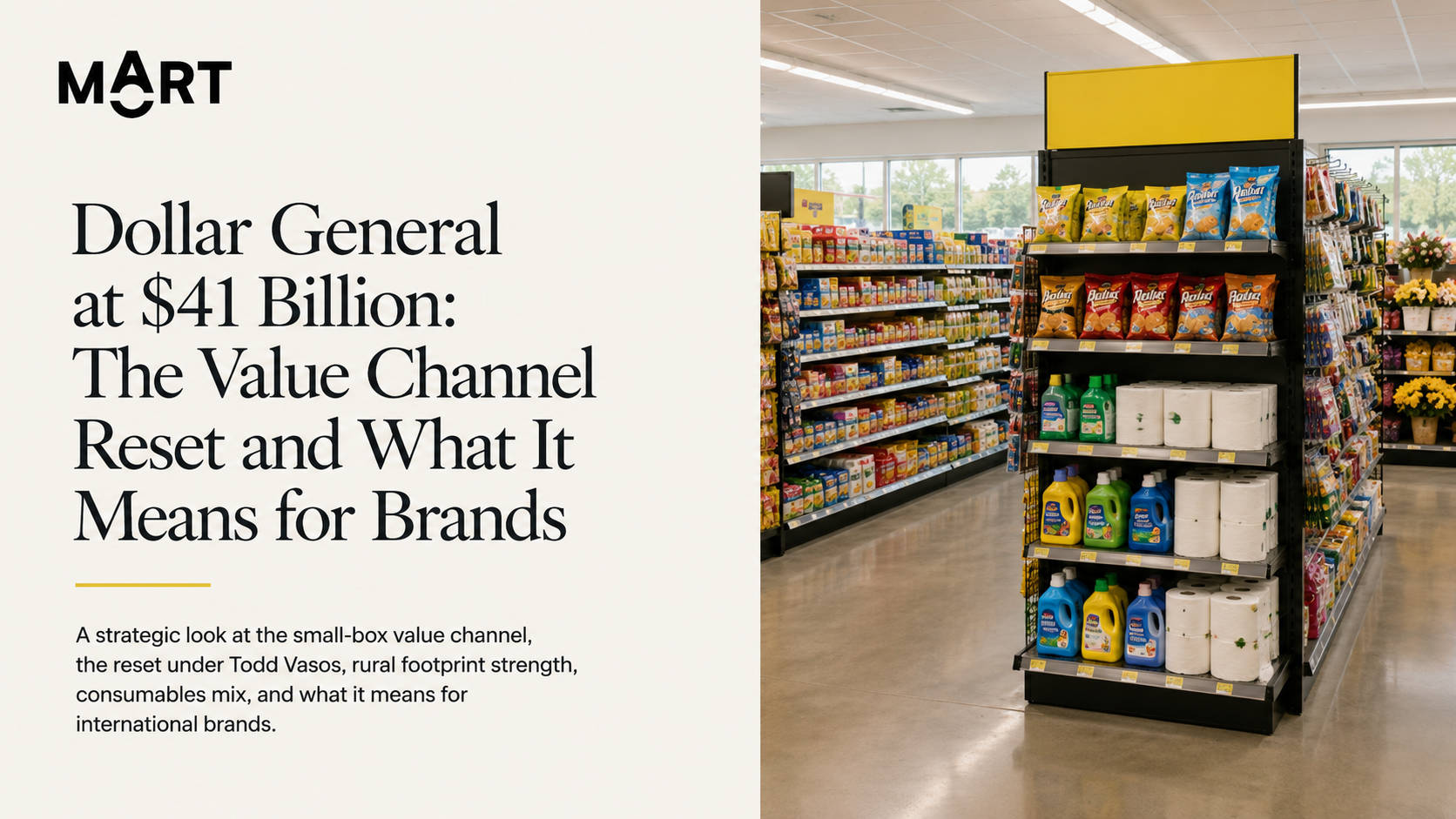

The store footprint and the rural advantage. Dollar General operates more than 20,000 stores, with the majority located in small towns and rural communities that have limited retail alternatives. The geographic footprint provides a structural advantage that is meaningfully difficult for competing retailers to replicate. For consumer brands seeking distribution into rural and small market geographies, Dollar General is often the single largest channel available, and the relationship has strategic value beyond the comparable sales math.

Category mix and the consumables emphasis. Approximately 80 percent of Dollar General sales come from consumables, including food, beverage, household, and personal care. The remaining 20 percent comes from seasonal, home, and apparel categories that carry meaningfully higher gross margins. The retailer's investment in fresh and frozen food through the DG Fresh program continued to expand category contribution. For brands in food and beverage, the Dollar General relationship can deliver substantial volume but requires SKU engineering for the small box format and the value price point.

What this means for international brands. Dollar General is best understood as a volume distribution channel for brands that have engineered product specifically for the small format and value price point. The relationship is operationally demanding, with carton specifications, palletization patterns, and EDI requirements that match large mass retail standards despite the small box format. Brands that can deliver an entry price point product engineered for the Dollar General shopper while maintaining margin structure tend to find the channel highly accretive. Brands that try to adapt premium products to the channel without engineering for it tend to find the economics challenging.